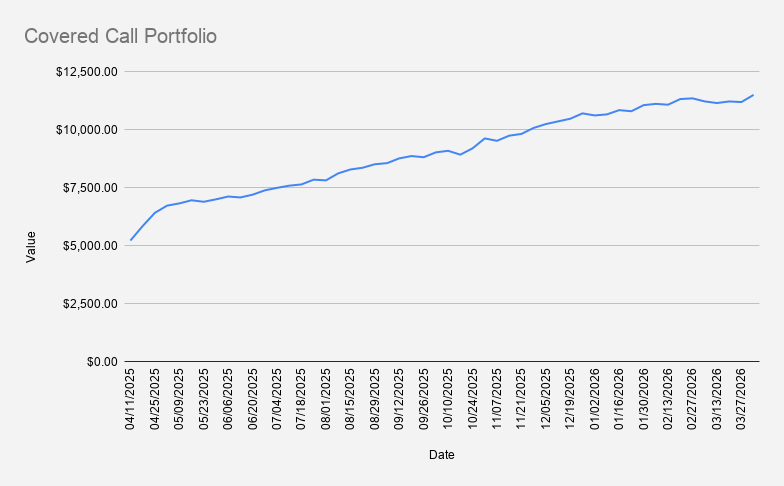

Portfolio Value: $11,491

Weekly Change: +2.76%

YTD Return: +11.14%

Options Premium Collected: $68

As of April 3, 2026, our options income portfolio increased by +2.76%, closing at $11,491.

The trading week was shortened ahead of Easter, while market sentiment remained heavily influenced by developments surrounding the conflict involving Iran. Energy prices, geopolitical uncertainty, and currency fluctuations continued to contribute to market volatility.

Because the portfolio is denominated in euros, it briefly exceeded the €10,000 mark several times during the week before finishing slightly below that level.

On a year-to-date basis, the portfolio is up 11.14%, outperforming both the S&P 500 (-4.16%) and NVDA (-6.74%) over the same period.

NVDA Recovery Supports Portfolio Growth

NVIDIA (NVDA) reclaimed the $170 level during the week, helping support overall portfolio performance.

The portfolio remains heavily concentrated in NVDA, which continues to serve as the primary engine for both capital appreciation and options income generation.

While concentration risk is always something to monitor, NVDA's liquidity and options market continue to make it an attractive candidate for premium-selling strategies.

Current Options Positions

- NVDA Apr 10, 2026 165/157.5 Bull Put Credit Spread

- 2x BMY Jun 18, 2026 50/46 Bull Put Credit Spread

- PFE May 15, 2026 25 Cash-Secured Put

- NVDA Nov 20, 2026 $120 Covered Call

Most of the portfolio's short-term premium continues to come from NVDA credit spreads, while Pfizer serves as a longer-term cash-secured put position.

For readers unfamiliar with these strategies, see:

- Bull Put Spread Strategy: A Complete Beginner's Guide

- Cash-Secured Puts Explained: A Complete Guide for Income Investors

Growing a Dividend Position With Options Income

One topic I spent some time thinking about this week was dividend income.

Because the portfolio remains relatively small and concentrated in growth-oriented positions, the current dividend stream is modest.

I briefly considered expanding into additional energy stocks to boost dividend income. However, after reviewing several candidates, I decided against introducing new positions solely for yield.

Instead, I chose to continue building an existing position in Pfizer (PFE).

The plan is straightforward:

- Gradually accumulate shares

- Use options premium to fund purchases

- Allow dividend income to grow organically over time

Rather than chasing high yields, I prefer building positions slowly and consistently.

During the week, premium generated from NVDA credit spreads was used to purchase:

- 0.1 shares of NVDA

- 0.5 shares of PFE

This reflects one of the core principles behind the portfolio: using options premium not only for immediate cash flow, but also as a tool for long-term portfolio growth.

Why I Continue Using Credit Spreads

As the portfolio evolves, I increasingly appreciate the capital efficiency of bull put spreads.

Compared to cash-secured puts, credit spreads allow me to define risk while requiring substantially less capital.

That flexibility becomes particularly valuable when managing a smaller portfolio and trying to balance income generation with diversification.

I compare both approaches in more detail here: Bull Put Spread vs Cash-Secured Put: Which Is Better for Small Accounts?.

Weekly Premium Income and Margin Debt

This week generated approximately $68 in options premium income.

A major objective remains reducing margin debt while maintaining a core holding of at least 100 NVDA shares.

Current margin debt stands at approximately -$3,474.

At a sustained pace of $68 per week, it would theoretically take around 52 weeks to eliminate the current margin balance.

The long-term goal remains unchanged: reduce and ideally eliminate margin debt without selling core positions.

Whether that happens during 2026 or later is less important than maintaining disciplined risk management throughout the process.

For more on realistic premium expectations, see: Can You Really Earn $100 Per Week Selling Options?.

Looking Ahead

The primary position to monitor next week is:

- NVDA Apr 10, 2026 165/157.5 Bull Put Credit Spread

If the position comes under pressure, the plan remains unchanged:

- Roll forward when appropriate

- Prefer collecting additional credit

- Prioritize long-term portfolio stability

I discuss my adjustment process in greater detail here: How to Manage a Credit Spread When the Trade Moves Against You.

Key Takeaway

This week reinforced an important investing principle: portfolio growth doesn't always require finding new opportunities.

Sometimes the best decision is to continue building existing positions, reinvesting premium income, and allowing compounding to do the heavy lifting.

Rather than chasing higher yields or introducing additional complexity, I chose to strengthen positions already in the portfolio and continue building both income and ownership over time.

Related Reading

- Bull Put Spread Strategy: A Complete Beginner's Guide

- Cash-Secured Puts Explained: A Complete Guide for Income Investors

- Bull Put Spread vs Cash-Secured Put: Which Is Better for Small Accounts?

- How to Manage a Credit Spread When the Trade Moves Against You

- Can You Really Earn $100 Per Week Selling Options?

Disclaimer

This trade journal reflects personal portfolio activity and is provided for educational and informational purposes only. It should not be considered investment advice, financial advice, tax advice, or a recommendation to buy or sell any security, option, derivative, or financial instrument. Options trading involves risk and may not be suitable for all investors.

Join the OptionsBrew newsletter

Get practical notes on options income, trade adjustments, and risk management.