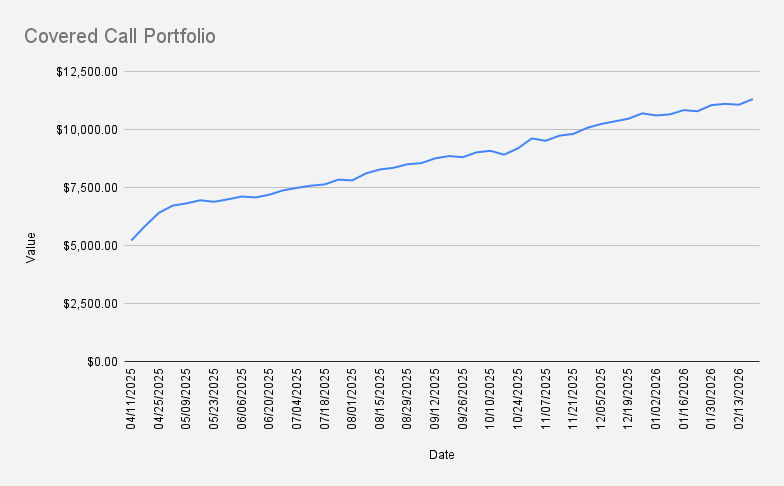

Portfolio Value: $11,312

Weekly Change: +2.20%

YTD Return: +6.91%

Options Premium Collected: $21.90

As of February 20, 2026, the portfolio increased by +2.20%, closing at $11,312.

Despite a relatively quiet week in terms of trading activity, portfolio growth remained intact. While much of my attention was focused on NVIDIA ahead of earnings, the position that ultimately required action was Pfizer (PFE).

Managing options positions often works that way. The trades you expect to require attention sometimes behave perfectly, while the quieter positions end up demanding adjustments.

Adding More McDonald's Shares

At the start of the week, I added another 0.1 shares of McDonald's (MCD) to the portfolio.

Over the past few years, we've developed a simple investing habit: whenever we visit McDonald's, I occasionally buy a small amount of MCD stock.

The goal isn't necessarily to build a large position quickly. Instead, it serves as a practical way to teach my daughter about ownership, investing, and how publicly traded businesses work.

I wrote more about this investing habit here: Why I Buy MCD Stock After Visiting McDonald's

Current Options Positions

- NVDA Feb 27, 2026 170/150 Bull Put Credit Spread

- 2x BMY Mar 20, 2026 50/46 Bull Put Credit Spread

- PFE Mar 13, 2026 26 Cash-Secured Put

- NVDA Jun 18, 2026 $116 Covered Call

The portfolio continues to rely primarily on three strategies:

- Bull Put Credit Spreads

- Cash-Secured Puts

- Covered Calls

Rolling the PFE Position

The primary adjustment this week involved Pfizer. As PFE approached my short strike, I decided to proactively adjust the position rather than wait for expiration.

The original position was a 26.5/25 bull put credit spread.

Rather than continuing to manage the spread structure, I converted the position into a cash-secured put at the 26 strike.

This adjustment generated enough additional premium to purchase another 0.5 shares of PFE, bringing the total PFE position to approximately one full share.

This illustrates one of the recurring themes of the portfolio:

Use options premium not only for income generation but also to gradually build ownership in productive assets.

For a complete guide to the strategy, see: Cash-Secured Puts Explained: A Complete Guide for Income Investors

The Trade-Off: More Flexibility, More Risk

Converting a credit spread into a cash-secured put is not without consequences.

The adjustment increases downside exposure because the long protective put is removed.

On the other hand, it also creates more flexibility for future adjustments and increases the probability that the trade ultimately works.

If PFE trades below $26, there remains a meaningful possibility that I will need to roll the position further.

This is one reason why I increasingly prefer defined-risk credit spreads when working with smaller portfolios.

I compare both approaches in detail here: Bull Put Spread vs Cash-Secured Put: Which Is Better for Small Accounts?

Preparing for NVDA Earnings

The major event on the horizon was NVIDIA earnings. At the time of writing, earnings had not yet been released, so uncertainty remained elevated.

While I felt reasonably optimistic heading into the report, experience has taught me that confidence and certainty are not the same thing. Options traders frequently underestimate how difficult earnings reactions can be to predict.

A company can beat expectations and still decline. Likewise, a disappointing report can sometimes lead to a rally.

For this reason, risk management remains more important than forecasting.

Weekly Options Income

This week generated approximately $21.90 in options premium income. That is significantly below some of the larger premium weeks we've experienced recently, but that's perfectly acceptable.

One of the biggest mistakes options traders make is feeling obligated to generate premium every single week. Sometimes preserving capital and avoiding unnecessary trades is the better decision.

I discuss realistic income expectations in greater detail here: Can You Really Earn $100 Per Week Selling Options?

Margin Debt Update

One of the primary objectives of the portfolio remains reducing margin debt while maintaining ownership of at least 100 NVDA shares. At the time of writing, margin debt stood at approximately -$3,943.

At a sustained pace of $21 per week, it would theoretically take around 187 weeks to eliminate the debt entirely.

Fortunately, not all weeks produce the same amount of premium.

The long-term objective remains straightforward:

- Generate recurring options income

- Reduce leverage gradually

- Preserve core stock positions

- Avoid unnecessary risk

Looking Ahead

The primary positions to monitor next week are:

- NVDA Feb 27, 2026 170/150 Bull Put Credit Spread

- PFE Mar 13, 2026 26 Cash-Secured Put

If either position comes under pressure, the management plan remains unchanged:

- Roll forward when appropriate

- Prefer collecting additional credit

- Prioritize long-term portfolio stability

I discuss my adjustment process in greater detail here: How to Manage a Credit Spread When the Trade Moves Against You

Key Takeaway

This week highlighted an important reality of options trading: not every week needs to be exciting.

The PFE adjustment improved the position, additional shares were accumulated, and the portfolio continued moving forward despite generating relatively modest premium.

Sometimes progress comes from collecting large premiums.

Other times it comes from patiently managing risk and avoiding unnecessary mistakes.

Related Reading

- Cash-Secured Puts Explained

- Bull Put Spread Strategy

- Bull Put Spread vs Cash-Secured Put

- Managing Challenged Credit Spreads

- Can You Really Earn $100 Per Week Selling Options?

- Why I Buy MCD Stock After Visiting McDonald's

Disclaimer

This trade journal reflects personal portfolio activity and is provided for educational and informational purposes only. It should not be considered investment advice, financial advice, tax advice, or a recommendation to buy or sell any security, option, derivative, or financial instrument. Options trading involves risk and may not be suitable for all investors. Past performance does not guarantee future results.

Join the OptionsBrew newsletter

Get practical notes on options income, trade adjustments, and risk management.