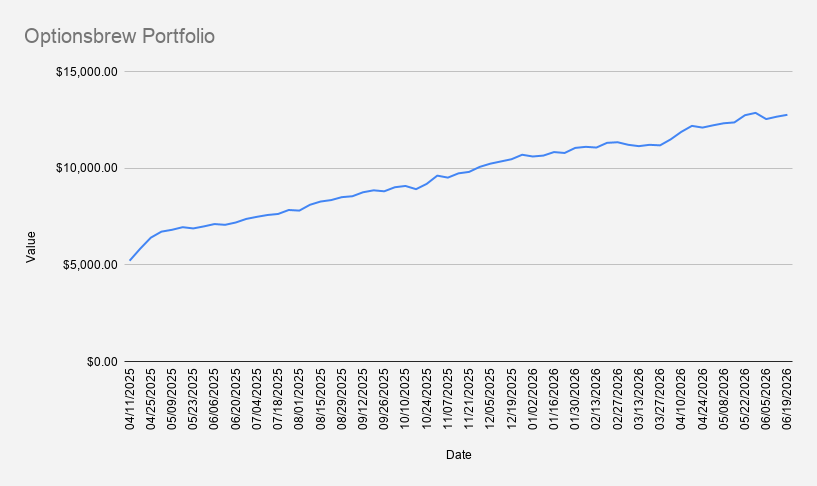

Portfolio Value: $12,761

Weekly Change: +0.76%

Options Premium Collected: $118

Margin Balance: -$2,890

As of June 19, 2026, the portfolio value increased by +0.76% compared to the previous week, reaching $12,761.

On a year-to-date basis, the portfolio is up 23.77%, outperforming both the S&P 500 (+9.36%) and NVIDIA (+11.56%). While comparing the portfolio to NVDA may seem unusual, it is a useful benchmark because approximately 84% of the portfolio's value is currently tied to NVIDIA. Given that concentration, I view outperforming NVDA itself as a positive sign that the options income strategy is adding value beyond simply holding the stock.

This was a shortened trading week for U.S. stocks, with markets closed on Friday, June 19, in observance of Juneteenth. As a European investor, it was interesting to learn more about the holiday. Juneteenth commemorates June 19, 1865, when enslaved African Americans in Texas were informed of their freedom after the Civil War. Today, U.S. stock markets close for the holiday.

Since the shorter trading week was known in advance, the portfolio's options positions were planned accordingly.

Rolling the NFLX Cash-Secured Put

The main portfolio adjustment this week was another roll of the Netflix (NFLX) cash-secured put.

The position was rolled to the January 15, 2027 expiration while improving the potential downside protection by approximately $600 and collecting additional premium.

This NFLX trade has already gone through several stages. It originally started as a weekly credit spread, later became a cash-secured put, and has now been rolled further out in time.

That makes it a useful example of how options trades can evolve when the underlying stock moves against the original thesis.

I wrote a full case study on this adjustment process here: How to Roll a Challenged Cash-Secured Put: An NFLX Case Study.

For readers unfamiliar with the strategy itself, see: Cash-Secured Puts Explained: A Complete Guide for Income Investors.

Why I Am Reducing the Number of Open Trades

Several longer-dated options positions expired this week, including Bristol-Myers Squibb (BMY) and Deutsche Bank on the Frankfurt exchange.

BMY was a position where I had been selling longer-dated credit spreads and using the premium to gradually buy shares of the stock itself. However, with the NFLX trade now requiring more attention and capital, I have decided to pause selling BMY options for a while.

That does not mean I am abandoning the stock. This week I still added a small amount of BMY to slightly increase future dividend income.

The Deutsche Bank position was more spontaneous. I originally opened it while visiting the Berlin Zoo with my daughter in April. The option expired worthless, and the portfolio kept the full premium in euros. For now, I am not planning to reopen the trade.

The current focus remains on NVDA and NFLX. I will continue selling weekly credit spreads where it makes sense, but I am also comfortable taking a slower pace during the summer.

Sometimes managing one or two positions carefully is better than opening several additional trades just to increase premium income.

Current Options Positions

- NVDA Jun 26, 2026 192.5/182.5 Bull Put Credit Spread

- LHA FRA Sep 18, 2026 7.6 Cash-Secured Put (EUR)

- ARCC Sep 18, 2026 16 Cash-Secured Put

- NFLX Jan 15, 2027 76 Cash-Secured Put

- NVDA Jun 17, 2027 $125 Covered Call

Most of the weekly premium strategy still comes from NVDA bull put spreads. NFLX is now more of a longer-dated cash-secured put position rather than a weekly income trade.

For more on why I often prefer credit spreads in smaller portfolios, see: Bull Put Spread Strategy: A Complete Beginner's Guide.

I also compare both strategies here: Bull Put Spread vs Cash-Secured Put: Which Is Better for Small Accounts?.

$118 in Weekly Options Premium

Total premium received this week from the NVDA credit spread and the NFLX roll was approximately $118.

That is a good result for the portfolio, especially considering the shortened trading week.

However, I do not expect every week to produce more than $100 in options premium. This week's result was helped by the NFLX roll, which is not something that can be repeated every week.

I continue to view $100 per week as a useful long-term target, but not something worth chasing aggressively.

For more on that topic, see: Can You Really Earn $100 Per Week Selling Options?.

Margin Debt Update

The portfolio margin balance decreased to approximately -$2,890.

In theory, if the portfolio generated $118 in premium every week, it would take about 25 weeks to eliminate the margin balance.

In practice, that is unlikely to happen in 2026. Not every week will produce more than $100 in premium, and part of the premium received is being reinvested into fractional shares.

The goal remains unchanged:

- Reduce margin debt gradually

- Avoid unnecessary leverage

- Maintain core positions

- Reinvest part of the premium into long-term holdings

Reinvesting Premium Into Shares

This week I added:

- 0.1 shares of NVDA

- 0.25 shares of BMY

The portfolio now holds approximately 8.25 shares of BMY.

The short-term goal is to gradually grow this position to 10 shares before deciding whether to allocate capital elsewhere.

One question I discussed with AI this week was whether to stop reinvesting into NVDA for a while and instead focus more on Apple (AAPL). That is something to think about for future portfolio construction, especially as I continue trying to balance growth exposure, dividend income, and concentration risk.

Looking Ahead

Next week, the primary position to watch is:

- NVDA Jun 26, 2026 192.5/182.5 Bull Put Credit Spread

If the position comes under pressure, the plan remains unchanged:

- Roll forward when appropriate

- Prefer collecting additional credit

- Prioritize portfolio stability over short-term premium targets

For more on this process, see: How to Manage a Credit Spread When the Trade Moves Against You.

Key Takeaway

This week reinforced an important lesson: premium income is useful, but portfolio simplicity also has value.

The NFLX roll helped push weekly premium above $100, but it also reminded me that managing challenged positions requires capital, attention, and patience.

For now, I am comfortable narrowing the focus to a smaller number of trades, mainly NVDA and NFLX, while continuing to reduce margin debt and reinvest part of the premium into long-term holdings.

Related Reading

- How to Roll a Challenged Cash-Secured Put: An NFLX Case Study

- Cash-Secured Puts Explained: A Complete Guide for Income Investors

- Bull Put Spread Strategy: A Complete Beginner's Guide

- Bull Put Spread vs Cash-Secured Put: Which Is Better for Small Accounts?

- How to Manage a Credit Spread When the Trade Moves Against You

- Can You Really Earn $100 Per Week Selling Options?

Disclaimer

This trade journal reflects personal portfolio activity and is provided for educational and informational purposes only. It should not be considered investment advice, financial advice, tax advice, or a recommendation to buy or sell any security, option, derivative, or financial instrument. Options trading involves risk and may not be suitable for all investors. Past performance does not guarantee future results.

Join the OptionsBrew newsletter

Get practical notes on options income, trade adjustments, and risk management.