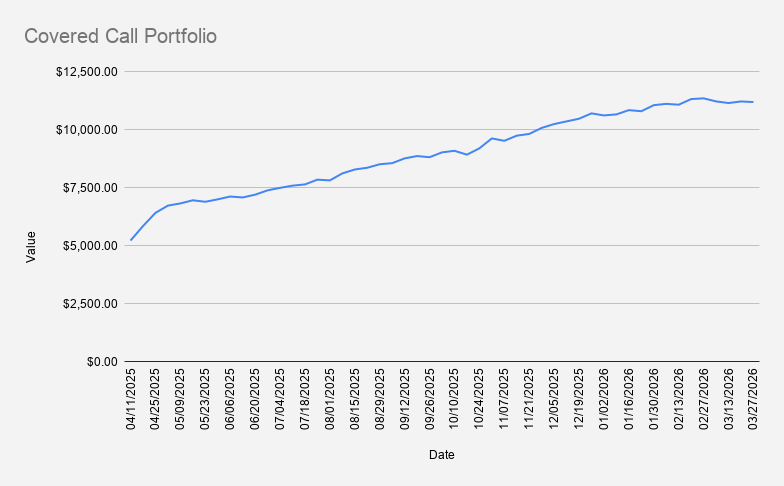

Portfolio Value: $11,183

Weekly Change: -0.24%

YTD Return: +8.50%

Options Premium Collected: $66

As of March 27, 2026, our options income portfolio declined slightly by -0.24%, closing at $11,183.

The decline was largely driven by currency fluctuations rather than weakness in the underlying positions. The U.S. dollar strengthened against the euro, trading around 1.15 EUR/USD. Since part of our reporting is euro-sensitive, exchange rate movements can materially affect portfolio valuations even when stock positions remain relatively stable.

On a year-to-date basis, the portfolio is up 8.50%, significantly outperforming both the S&P 500 (-7.14%) and NVDA (-11.29%) over the same period.

Market Volatility Returns as NVDA Pulls Back

Broader markets experienced increased volatility during the week, with NVIDIA (NVDA) trading below the $170 level for the first time in several weeks.

The move appeared to be driven largely by geopolitical concerns surrounding the Middle East and growing fears of disruptions to global energy supplies. Reports discussing a potential blockade of the Strait of Hormuz pushed oil prices above $110 per barrel and increased uncertainty across equity markets.

While headlines often dominate short-term price action, my focus remains on managing positions rather than attempting to predict geopolitical outcomes.

As an options seller, periods of increased volatility can actually create opportunities because option premiums tend to expand. The challenge is balancing premium collection against the risk of larger market moves.

Current Options Positions

- NVDA Apr 3, 2026 160/150 Bull Put Credit Spread

- 2x BMY Jun 18, 2026 50/46 Bull Put Credit Spread

- PFE May 15, 2026 25 Cash-Secured Put

- NVDA Nov 20, 2026 $120 Covered Call

The portfolio continues to rely on a combination of credit spreads, cash-secured puts, and covered calls to generate recurring income while maintaining exposure to long-term holdings.

If you're unfamiliar with these strategies, start here:

- Bull Put Spread Strategy: A Complete Beginner's Guide

- Cash-Secured Puts Explained: A Complete Guide for Income Investors

Using Credit Spreads to Generate Income

The primary source of premium income this week remained NVDA bull put spreads.

One reason I prefer credit spreads for a portfolio of this size is their capital efficiency. Compared to cash-secured puts, they require substantially less buying power while keeping risk defined from the start.

This allows me to continue generating premium income without concentrating too much capital into a single position.

For a detailed comparison of both approaches, see: Bull Put Spread vs Cash-Secured Put: Which Is Better for Small Accounts?.

Reinvesting Premium Into Long-Term Holdings

Using premium collected from NVDA credit spreads, I added another 0.1 shares of NVDA, bringing the total position to approximately 101.6 shares.

This remains one of the core ideas behind the portfolio.

Rather than treating options income purely as cash flow, I use part of the premium to gradually increase ownership of productive assets.

Over time, even small additions can compound into meaningful positions.

Weekly Premium Income and Margin Debt

This week generated approximately $66 in options premium income.

A major objective remains reducing margin debt while maintaining a core holding of at least 100 NVDA shares.

Current margin debt stands at approximately -$3,508.

At a sustained pace of $66 per week, it would theoretically take around 52 weeks to eliminate the current margin balance.

The goal remains straightforward: gradually reduce leverage without selling core positions or taking unnecessary risks.

Whether that happens during 2026 or extends into 2027 is ultimately less important than maintaining discipline and consistency.

I discuss realistic income expectations in more detail here: Can You Really Earn $100 Per Week Selling Options?.

Looking Ahead

The primary position to monitor next week is:

- NVDA Apr 3, 2026 160/150 Bull Put Credit Spread

If the position comes under pressure, the management plan remains unchanged:

- Roll forward when appropriate

- Prefer collecting additional credit

- Maintain long-term portfolio stability

I explain my adjustment process in greater detail here: How to Manage a Credit Spread When the Trade Moves Against You.

Key Takeaway

This week demonstrated that portfolio performance is influenced by more than just stock prices.

Currency movements, geopolitical developments, and market sentiment all play a role in short-term results. However, none of those factors changed the long-term plan.

The strategy remains simple: generate premium income, reinvest part of that income into long-term holdings, reduce margin debt gradually, and manage risk conservatively.

In volatile markets, consistency often matters more than prediction.

Related Reading

- Bull Put Spread Strategy: A Complete Beginner's Guide

- Cash-Secured Puts Explained: A Complete Guide for Income Investors

- Bull Put Spread vs Cash-Secured Put: Which Is Better for Small Accounts?

- How to Manage a Credit Spread When the Trade Moves Against You

- Can You Really Earn $100 Per Week Selling Options?

Disclaimer

This trade journal reflects personal portfolio activity and is provided for educational and informational purposes only. It should not be considered investment advice, financial advice, tax advice, or a recommendation to buy or sell any security, option, derivative, or financial instrument. Options trading involves risk and may not be suitable for all investors. Past performance does not guarantee future results.

Join the OptionsBrew newsletter

Get practical notes on options income, trade adjustments, and risk management.