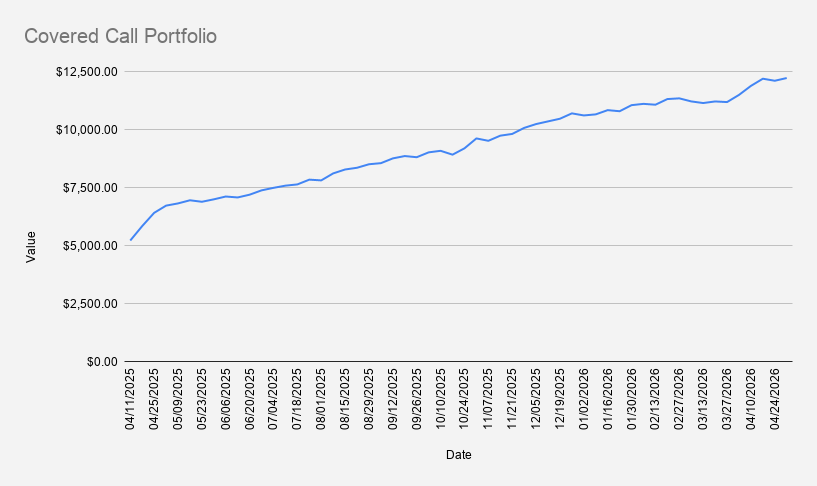

Portfolio Value: $12,218

Weekly Change: +0.97%

YTD Return: +15.48%

Options Premium Collected: $58

As of May 1, 2026, the portfolio increased by +0.97%, closing at $12,218.

While many investors dislike seeing their stocks decline, this week offered a useful reminder that options sellers often benefit from a different perspective.

After rallying above $210, NVIDIA (NVDA) pulled back below $200. For a premium seller, this was not necessarily bad news. Strong rallies often compress option premiums, making it harder to establish attractive new positions. A moderate pullback can improve risk-reward opportunities while also reducing the likelihood of chasing extended price action.

This is one reason why options trading and traditional investing sometimes lead to different reactions to the same market move.

On a year-to-date basis, the portfolio is now up 15.48%, outperforming both the S&P 500 (+5.71%) and NVDA (+5.87%) over the same period.

Using Bull Put Spreads on NVDA

Following the pullback, I opened a new NVIDIA bull put credit spread:

NVDA May 8, 2026 187.5/177.5 Bull Put Credit Spread

The objective remains straightforward: generate premium income while maintaining defined risk.

Rather than attempting to predict short-term market direction, I focus on establishing positions with a high probability of success and managing them actively if market conditions change.

For readers unfamiliar with the strategy, see: Bull Put Spread Strategy: A Complete Beginner's Guide to Selling Credit Spreads for Income

One advantage of bull put spreads is that they allow premium collection without committing the capital required for a traditional cash-secured put.

For a deeper comparison, see: Bull Put Spread vs Cash-Secured Put: Which Is Better for Small Accounts?

Current Options Positions

- NVDA May 8, 2026 187.5/177.5 Bull Put Credit Spread

- 2x BMY Jun 18, 2026 50/46 Bull Put Credit Spread

- PFE May 15, 2026 25 Cash-Secured Put

- DBK FRA Jun 19, 2026 24/20 Bull Put Credit Spread

- NVDA Nov 20, 2026 $120 Covered Call

Reinvesting Premium Into Ownership

Using premium collected from the NVDA credit spread, I added another 0.1 shares of NVDA.

This reflects one of the core principles behind the portfolio.

Rather than treating options income solely as cash flow, I use part of the premium to gradually increase ownership of productive assets.

The portfolio now holds approximately 102.1 shares of NVDA.

Small additions may seem insignificant individually, but repeated consistently over time they can contribute meaningfully to long-term portfolio growth.

Weekly Income vs Risk Management

This week generated approximately $58 in options premium income.

While that falls short of my long-term objective of generating roughly $100 per week in premium income, I intentionally resisted the temptation to force additional trades.

One of the easiest mistakes options traders make is increasing position size simply to hit an income target.

Additional premium often comes with additional risk.

In this case, opening more positions would have increased portfolio exposure without meaningfully improving the quality of the trade setup.

Sometimes the best trade is the one you decide not to take.

I discuss the $100 weekly income goal in more detail here: Can You Really Earn $100 Per Week Selling Options?

Margin Debt Update

One of the portfolio's ongoing objectives is reducing margin debt while maintaining a core holding of 100 NVDA shares.

Current margin debt stands at approximately -$3,357.

At a sustained pace of $58 per week in premium income, it would theoretically take roughly 58 weeks to eliminate the balance.

Realistically, premium income fluctuates, market conditions change, and portfolio adjustments become necessary. Because of that, I am comfortable extending the debt-reduction timeline into 2027 if required.

Preserving capital and maintaining flexibility remain more important than forcing an aggressive repayment schedule.

Lessons From This Week

- Pullbacks can create better opportunities for premium sellers than extended rallies.

- Risk management matters more than hitting arbitrary income targets.

- Reinvesting premium helps gradually increase portfolio ownership.

- Patience is often a competitive advantage in options trading.

Looking Ahead

The primary position to monitor next week is the NVDA 187.5/177.5 bull put spread.

I will also need to make a decision regarding the Pfizer cash-secured put approaching expiration.

If any position comes under pressure, the plan remains unchanged:

- Roll when appropriate

- Prefer collecting additional credit

- Prioritize portfolio stability over short-term perfection

For more on my trade adjustment process, see: How to Manage a Credit Spread When the Trade Moves Against You

Key Takeaway

This week reinforced a lesson that many options traders eventually learn:

The goal is not maximizing premium every week.

The goal is building a repeatable process that balances income generation, risk management, and long-term portfolio growth.

Sometimes that means opening new positions. Sometimes it means waiting patiently and avoiding unnecessary trades.

Over time, both decisions can contribute to successful outcomes.

Related Reading

- Bull Put Spread Strategy: A Complete Beginner's Guide

- Bull Put Spread vs Cash-Secured Put: Which Is Better for Small Accounts?

- Can You Really Earn $100 Per Week Selling Options?

- How to Manage a Credit Spread When the Trade Moves Against You

Disclaimer

This trade journal reflects personal portfolio activity and is provided for educational and informational purposes only. It should not be considered investment advice, financial advice, tax advice, or a recommendation to buy or sell any security, option, derivative, or financial instrument. All investments involve risk, including the possible loss of principal.

Join the OptionsBrew newsletter

Get practical notes on options income, trade adjustments, and risk management.