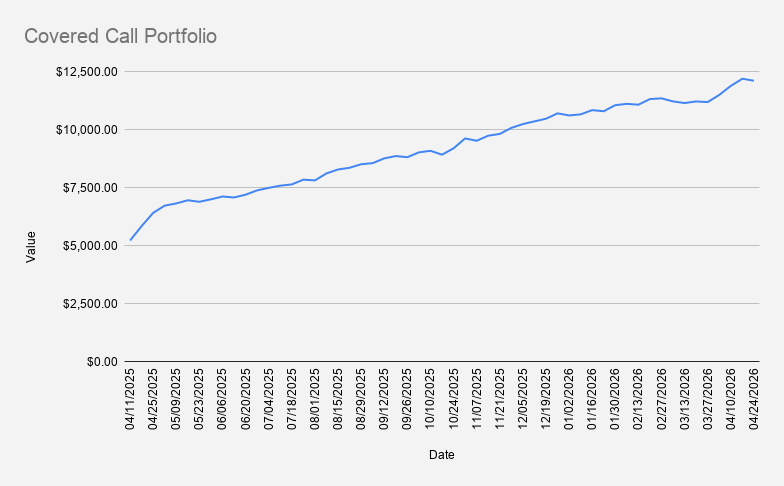

Portfolio Value: $12,101

Weekly Change: -0.72%

YTD Return: +15.38%

Options Premium Collected: $67

As of April 24, 2026, the portfolio decreased slightly by -0.72%, closing at $12,101.

Since the portfolio is euro-sensitive, part of the decline was caused by currency movement. The U.S. dollar strengthened against the euro, with EUR/USD trading around 1.17. For international investors, exchange rates can affect reported portfolio value even when the underlying positions remain broadly intact.

On a year-to-date basis, the portfolio is still up 15.38%, outperforming both the S&P 500 (+4.43%) and NVDA (+10.87%) over the same period.

NVDA Above $200: Why Strong Rallies Can Be Difficult for Put Sellers

NVIDIA (NVDA) moved well above $200 this week, creating a familiar challenge for options sellers.

As a put seller, I am always cautious after strong rallies. While rising stock prices are generally good for existing long positions, they can make new premium-selling trades less attractive.

When a stock moves sharply higher, put premiums often become less appealing while the risk of a sudden pullback increases. That makes it harder to structure conservative cash-secured puts or bull put credit spreads with enough margin of safety.

Still, NVDA remains the anchor position in the portfolio, so I continued the weekly premium strategy using a defined-risk bull put credit spread.

If you're unfamiliar with the strategy, see: Bull Put Spread Strategy: A Complete Beginner's Guide to Selling Credit Spreads for Income.

Current Options Positions

- NVDA May 1, 2026 195/185 Bull Put Credit Spread

- 2x BMY Jun 18, 2026 50/46 Bull Put Credit Spread

- PFE May 15, 2026 25 Cash-Secured Put

- DBK FRA Jun 19, 2026 24/20 Bull Put Credit Spread

- NVDA Nov 20, 2026 $120 Covered Call

The primary position to monitor remains the NVDA 195/185 bull put spread. If the stock experiences a larger pullback and the position comes under pressure, the plan remains unchanged: roll forward when appropriate and ideally collect additional premium in the process.

For more on my adjustment process, see: How to Manage a Credit Spread When the Trade Moves Against You.

Reinvesting Premium Into NVDA Shares

Using premium collected from NVDA credit spreads, I added another 0.1 shares of NVDA.

The approach remains consistent: use options income not only for short-term cash flow but also to gradually increase ownership of productive assets.

The portfolio now holds approximately 102 shares of NVDA.

This remains one of the core ideas behind the portfolio. Options premium can generate income today while simultaneously helping build larger positions for the future.

Weekly Options Income and Margin Management

This week generated approximately $67 in options premium income.

One of the portfolio's primary objectives remains reducing margin debt while preserving a core holding of at least 100 NVDA shares.

Current margin debt stands at approximately -$3,398.

At a sustained pace of $67 per week, it would theoretically take around 50 weeks to eliminate the margin balance entirely.

Of course, markets rarely move in straight lines. Premium income fluctuates, assignments happen, and opportunities appear unexpectedly. Because of that, I am comfortable extending the debt-reduction timeline into 2027 if necessary.

The objective is not speed. The objective is survival, consistency, and gradual portfolio improvement.

I discuss realistic weekly premium expectations in more detail here: Can You Really Earn $100 Per Week Selling Options?.

Why I Avoided Adding More Positions

During the week, I considered opening additional positions in an attempt to move weekly premium income closer to the $100 target.

Ultimately, I decided against it.

One of the easiest mistakes options traders make is forcing trades simply to meet an income goal. More premium usually means more risk, and in this case, the available opportunities did not justify the additional exposure.

Sometimes the best trade is the one you don't take.

Maintaining discipline is often more important than squeezing out an extra few dollars of premium.

Credit Spreads vs Cash-Secured Puts

This week also reinforced why I often prefer bull put spreads over cash-secured puts in smaller portfolios.

A cash-secured put on a stock such as NVDA requires significant capital. A defined-risk spread allows me to generate income while preserving buying power and maintaining diversification.

Both strategies have advantages, but for many smaller accounts, credit spreads can offer a more capital-efficient way to pursue premium income.

For a detailed comparison, see: Bull Put Spread vs Cash-Secured Put: Which Is Better for Small Accounts?.

Portfolio Performance and Risk Control

An interesting observation is that the portfolio currently generates roughly one-third to one-half of the premium income it produced a year ago.

While that might sound disappointing, I actually view it as a positive development.

Lower premium income often reflects lower risk exposure.

This week's return on capital was approximately 0.47%. While that falls short of the 1% weekly target I once pursued, it remains a respectable result achieved with a much more conservative risk profile.

Over time, consistency tends to outperform aggressiveness.

Looking Ahead

Next week's primary focus remains the NVDA 195/185 bull put spread.

I will also need to make a decision regarding the Pfizer cash-secured put approaching expiration on May 15.

If any position comes under pressure, the plan remains straightforward:

- Roll when appropriate

- Prefer collecting additional credit

- Prioritize portfolio stability over short-term income goals

Key Takeaway

This week reinforced an important lesson for income-focused investors:

Strong rallies are not always easy environments for options sellers.

While rising stock prices benefit long-term holdings, they can make new premium-selling opportunities less attractive and increase the temptation to chase risk.

For this portfolio, the goal remains unchanged: generate recurring options income, reinvest part of that income into productive assets, reduce leverage gradually, and avoid unnecessary risk.

Related Reading

- Bull Put Spread Strategy: A Complete Beginner's Guide

- Bull Put Spread vs Cash-Secured Put: Which Is Better for Small Accounts?

- How to Manage a Credit Spread When the Trade Moves Against You

- Can You Really Earn $100 Per Week Selling Options?

Disclaimer

This trade journal reflects personal portfolio activity and is provided for educational and informational purposes only. It should not be considered investment advice, financial advice, tax advice, or a recommendation to buy or sell any security, option, derivative, or financial instrument. Options trading involves risk and may not be suitable for all investors. All investments involve the possible loss of principal.

Join the OptionsBrew newsletter

Get practical notes on options income, trade adjustments, and risk management.