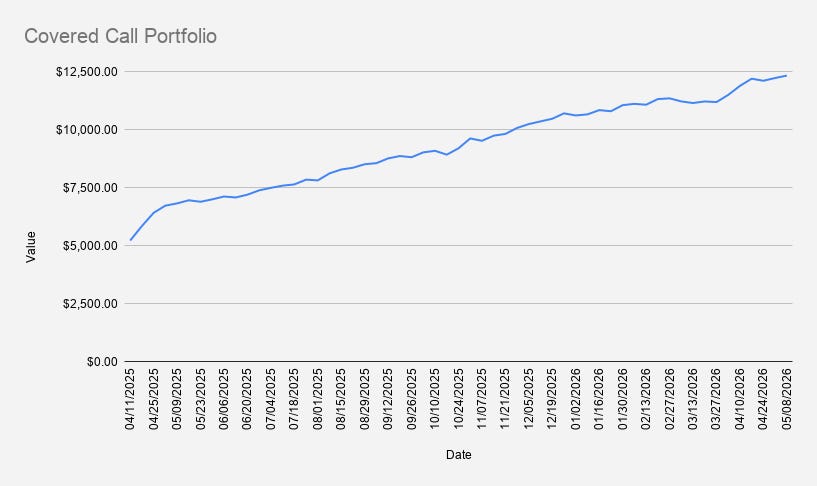

Portfolio Value: $12,323

Weekly Change: +0.86%

YTD Return: +16.51%

Options Premium Collected: $89

As of May 8, 2026, the portfolio increased by +0.86%, reaching $12,323.

On a year-to-date basis, the portfolio is now up 16.51%, outperforming both the S&P 500 (+7.88%) and NVDA (+13.98%) over the same period.

Continuing the NVDA Credit Spread Strategy

NVIDIA (NVDA) continued its impressive rally this week, trading above $215 per share. As a result, the previous week's bull put spread expired worthless, allowing the portfolio to retain the entire premium collected.

Despite the strong move higher, I decided to continue the strategy and opened a new NVDA bull put credit spread for the following week's expiration.

One challenge with selling premium after a large rally is that the probability of a short-term pullback often increases. While the trend may remain bullish, option sellers must constantly balance premium collection against downside risk.

This is one reason why I prefer defined-risk strategies such as bull put spreads rather than relying entirely on cash-secured puts.

If you're unfamiliar with the mechanics of this strategy, see:

Bull Put Spread Strategy: A Complete Beginner's Guide to Selling Credit Spreads for Income

The Goal: Consistent Weekly Premium Income

One of the long-term goals of this portfolio is generating approximately $100 per week in options premium while maintaining reasonable risk levels.

At the current portfolio size, that target appears achievable, but it requires careful position selection.

The challenge isn't finding stocks with liquid options. The challenge is finding stocks I would also be comfortable owning or managing through difficult market conditions.

For smaller portfolios, capital efficiency and risk management often matter more than maximizing premium on any single trade.

I discuss the math behind this goal in more detail here:

Can You Really Earn $100 Per Week Selling Options?

Adding ARCC Through a Cash-Secured Put

This week I introduced a new position: Ares Capital Corporation (ARCC).

ARCC is primarily known as an income-oriented stock with a relatively high dividend yield. I previously owned shares in a dividend-focused portfolio and have generally viewed it as a cash-flow-oriented investment rather than a growth stock.

Because liquid options are available, I decided to sell a cash-secured put with a September expiration.

Unlike weekly credit spreads, this position is designed to generate income while potentially creating an opportunity to acquire additional shares at a lower price.

This highlights one of the key differences between credit spreads and cash-secured puts:

Bull Put Spread vs Cash-Secured Put: Which Is Better for Small Accounts?

Current Options Positions

- NVDA May 15, 2026 202.5/192.5 Bull Put Credit Spread

- 2x BMY Jun 18, 2026 50/46 Bull Put Credit Spread

- PFE May 15, 2026 25 Cash-Secured Put

- DBK FRA Jun 19, 2026 24/20 Bull Put Credit Spread

- ARCC Sep 18, 2026 16 Cash-Secured Put

- NVDA Nov 20, 2026 $120 Covered Call

Reinvesting Premium Into Ownership

Using premium collected from the NVDA credit spread and the ARCC cash-secured put, I purchased:

- 0.1 shares of NVDA

- 1 share of ARCC

This remains one of the central ideas behind the portfolio.

Options income is not only used for short-term cash flow. A portion of the premium is regularly reinvested into long-term holdings, allowing the portfolio to compound gradually over time.

As a result of these additions, projected annual dividend income increased to approximately $63.43.

While that amount remains relatively small, the objective is creating a system where options premium finances portfolio growth without requiring constant capital contributions.

Weekly Premium Income and Margin Management

This week generated approximately $89 in options premium income.

That figure brings the portfolio closer to the long-term goal of generating $100 per week on a relatively consistent basis.

However, one lesson I've learned repeatedly is that increasing premium income by taking excessive risk rarely ends well.

Options trading rewards consistency far more than aggressiveness.

At the current margin balance of approximately -$3,324, maintaining an average pace of $89 per week would theoretically eliminate the debt within roughly 38 weeks.

Realistically, market conditions change, premiums fluctuate, and unexpected adjustments become necessary. For that reason, I am comfortable extending the debt-reduction timeline into 2027 if needed.

The priority remains preserving capital while steadily improving the portfolio's financial position.

Looking Ahead

Next week's primary focus remains the NVDA 202.5/192.5 bull put spread.

If the position comes under pressure, the plan remains unchanged:

- Roll forward when appropriate

- Prefer collecting additional premium

- Maintain disciplined risk management

If the Pfizer put expires worthless, I may reallocate capital into another liquid weekly options candidate.

One stock currently under consideration is Netflix (NFLX), which could potentially become a second weekly premium generator alongside NVDA.

The objective is diversification, not simply collecting more premium.

Key Takeaway

This week reinforced an important lesson for income-focused investors.

Generating options income is only part of the process. Long-term success comes from balancing premium generation, portfolio growth, diversification, and risk management.

Whether through bull put spreads, cash-secured puts, or covered calls, the goal remains the same: create a repeatable process that can generate income while steadily building long-term ownership.

Related Reading

- Bull Put Spread Strategy: A Complete Beginner's Guide

- Bull Put Spread vs Cash-Secured Put: Which Is Better for Small Accounts?

- Can You Really Earn $100 Per Week Selling Options?

- How to Manage a Credit Spread When the Trade Moves Against You

Disclaimer

This trade journal reflects personal portfolio activity and is provided for educational and informational purposes only. It should not be considered investment advice, financial advice, tax advice, or a recommendation to buy or sell any security, option, derivative, or financial instrument. All investments involve risk, including the possible loss of principal.

Join the OptionsBrew newsletter

Get practical notes on options income, trade adjustments, and risk management.