This week was all about managing positions after NVDA earnings, collecting another round of options premium, and continuing to grow the underlying stock portfolio.

While NVDA's earnings were strong, the market's reaction was relatively muted. The stock pulled back slightly after the announcement, which is often where option sellers can find opportunities. Since most of my short-term income comes from selling bull put spreads and covered calls, a modest decline isn't necessarily bad news.

In fact, lower volatility after earnings often helps short option positions.

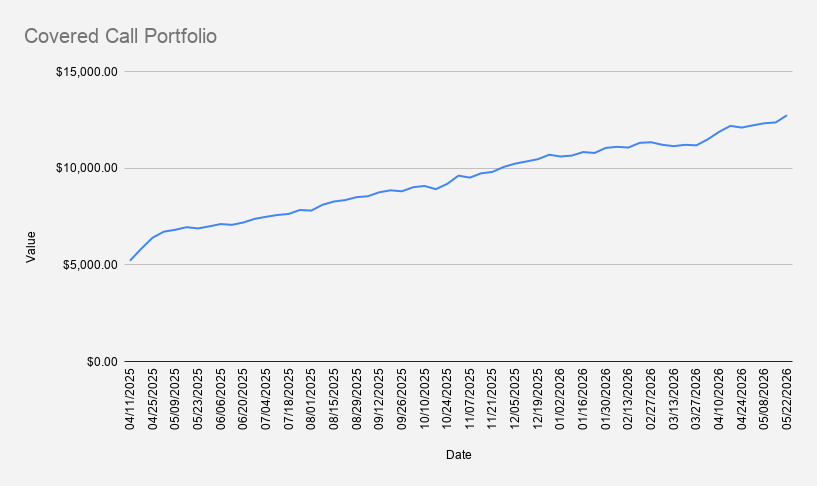

As of May 22, 2026, the portfolio value stands at $12,740, representing a 22.48% gain year-to-date. For comparison, the S&P 500 has returned approximately 9.26% this year, while NVDA itself is up 15.39%.

Why NVDA Remains My Primary Options Income Vehicle

I continue to focus most of my options activity around NVDA for one simple reason: liquidity.

With NVDA now one of the largest companies in the world, its options market is incredibly active. High liquidity generally means tighter bid-ask spreads, easier fills, and more flexibility when positions need to be adjusted.

For income-focused trading, that's a major advantage.

This week I considered expanding into names such as AAPL and PLTR, but ultimately decided against it. At the current portfolio size, I don't see much benefit in adding exposure simply for the sake of diversification.

Instead, I prefer concentrating on a few highly liquid names that I understand well.

Adding NFLX to the Rotation

One change this week was adding NFLX credit spreads.

The goal isn't to replace NVDA but to introduce another high-quality underlying that offers attractive option premiums.

Compared to NVDA, NFLX typically requires accepting slightly lower probabilities of success to generate similar premium income. While some NVDA positions can be structured with theoretical probabilities above 90%, NFLX often falls into the mid-to-high 80% range.

That's still acceptable for me, provided position sizing remains conservative.

As always, the objective isn't maximizing premium. The objective is generating repeatable income while keeping risk manageable.

Current Options Positions

The portfolio currently holds the following options positions:

- NVDA May 29, 2026 205/195 Bull Put Credit Spread

- NFLX May 29, 2026 85/80 Bull Put Credit Spread

- 2x BMY Jun 18, 2026 50/46 Bull Put Credit Spread

- DBK FRA Jun 19, 2026 24/20 Bull Put Credit Spread

- ARCC Sep 18, 2026 16 Cash-Secured Put

- NVDA Jun 17, 2027 $125 Covered Call

All weekly positions from the previous cycle expired worthless, allowing me to keep the full premium and deploy capital into new trades.

That's exactly the outcome I'm seeking with these short-duration spreads.

Converting Options Premium Into Long-Term Assets

One of the core ideas behind this portfolio is that options income doesn't simply sit in cash.

Instead, I use the premium generated from trades to gradually acquire additional shares of companies I want to hold long term.

This week the options premium funded purchases of:

- 0.1 shares of McDonald's (MCD)

- 0.1 shares of Netflix (NFLX)

- 0.1 shares of Nvidia (NVDA)

- 0.5 shares of Pfizer (PFE)

These purchases may appear small, but they accumulate over time.

My goal isn't to make a life-changing purchase every week. The goal is to consistently convert short-term premium income into long-term assets.

Dividend Income Continues to Climb

The dividend side of the portfolio also moved higher this week.

The new purchases increased projected annual dividend income by approximately $1.31.

That may not sound impressive on its own, but small increases repeated week after week can become meaningful over time.

I also noticed that Deutsche Bank is approaching its annual dividend payment. With 26 shares currently held, the portfolio's projected annual dividend income has now climbed to roughly $90 per year.

The next milestone is obvious: pushing annual dividend income above $100.

It's not a large number, but it represents another step toward building a self-sustaining income portfolio.

Premium Income and Margin Reduction

Options generated $66.90 in premium income this week.

While I would certainly like to see weekly premium consistently exceed $100, I'm not willing to take substantially more risk just to reach that target.

The portfolio still carries approximately $3,135 in margin debt, and reducing that balance remains one of my priorities.

At the current pace, eliminating the debt will take time. That's fine.

I would rather move slowly with controlled risk than aggressively chase returns and expose the portfolio to unnecessary drawdowns.

What I'm Watching Next Week

The primary positions on my radar remain:

- NVDA 205/195 Bull Put Credit Spread

- NFLX 85/80 Bull Put Credit Spread

If either position comes under pressure, my preferred adjustment remains the same as always: roll forward whenever possible, ideally for a net credit.

One of the advantages of trading highly liquid names is that adjustments are usually available before positions become problematic.

The goal isn't avoiding every losing trade.

The goal is managing risk well enough that a single trade never becomes a portfolio-threatening event.

Portfolio Principles

As the portfolio grows, the underlying philosophy remains unchanged:

- Generate recurring options premium

- Focus on highly liquid stocks

- Use defined-risk strategies whenever possible

- Reinvest premium into long-term holdings

- Increase dividend income over time

- Reduce margin debt responsibly

- Prioritize capital preservation over maximizing returns

Twenty-two percent returns are nice.

But the long-term objective is not a single good year.

The objective is building a portfolio that can continue producing income and compounding capital for years to come.

Disclaimer: This article reflects personal portfolio activity and market observations for informational and educational purposes only. It does not constitute financial advice, investment advice, tax advice, or a recommendation to buy or sell any securities, derivatives, or financial instruments.

Options trading involves substantial risk and may not be suitable for all investors. Past performance does not guarantee future results. Always conduct your own research and consult a qualified financial professional before making investment decisions.

Join the OptionsBrew newsletter

Get practical notes on options income, trade adjustments, and risk management.